Avocados we buy at supermarkets almost certainly begin their journey at a family farm in Mexico. From there, a packaging company purchases these agricultural products, sorts them, and then ships them to the United States. Once in the U.S., distributors transport them to grocery stores in our towns. When we spend a dollar on that avocado, it has likely passed through the hands of four companies, each competing with several others for a share of the fruit market. This dollar covers all costs: cultivation, packaging, transportation, display, and checkout at the cash register.

Renowned British economist Friedrich Hayek (1899-1992) believed that this competition is the lifeblood of a healthy economic system. He referred to it as the most efficient way to provide goods to consumers.

Now, let’s think about products more closely related to us, such as life-sustaining medications taken by an elderly person to control a chronic disease. These medications are produced by pharmaceutical companies. Subsequently, they are typically sold to drug benefit management organizations, then transported to retail pharmacies, prescribed by doctors, and mostly paid for by insurance companies, Medicare, or Medicaid.

Similar to avocados, these pills change hands multiple times. However, the crucial distinction lies in the fact that in this scenario, the drugs may go from the factory to the pharmacy counter with each step possibly belonging to the same huge healthcare company. Even the doctor prescribing the medication could be an employee of this company.

Users may pay a $15 copayment, but this is only a small portion of the visible cost. The rest is paid by a large company – most of the money lines its own pockets, ultimately coming from employers or taxpayers.

This is vertical integration – an entity controlling almost the entire supply chain.

Today, nearly all Americans obtain prescription drugs from a few companies, often encompassing more healthcare services as well. These companies almost monopolize every aspect from production to consumption, including payment itself.

Some experts believe that the vertical integration model is a win-win overall. By streamlining the supply chain, these large enterprises can reduce waste, enhance convenience, and lower prices for patients, while simultaneously reaping substantial profits themselves.

Others hold a different view. They argue that vertical integration stifles competition, enabling a few companies to dictate prices to manufacturers and consumers. Some point out that this practice reduces patient choices, as these companies steer patients towards their services and drive up the cost of life-sustaining medications.

So, which scenario is it?

Let’s delve deeper into how large corporations shape the healthcare market and impact taxpayers using the case of UnitedHealth Group, the world’s largest healthcare company headquartered in Minnetonka, Minnesota, and the third-largest in the U.S.

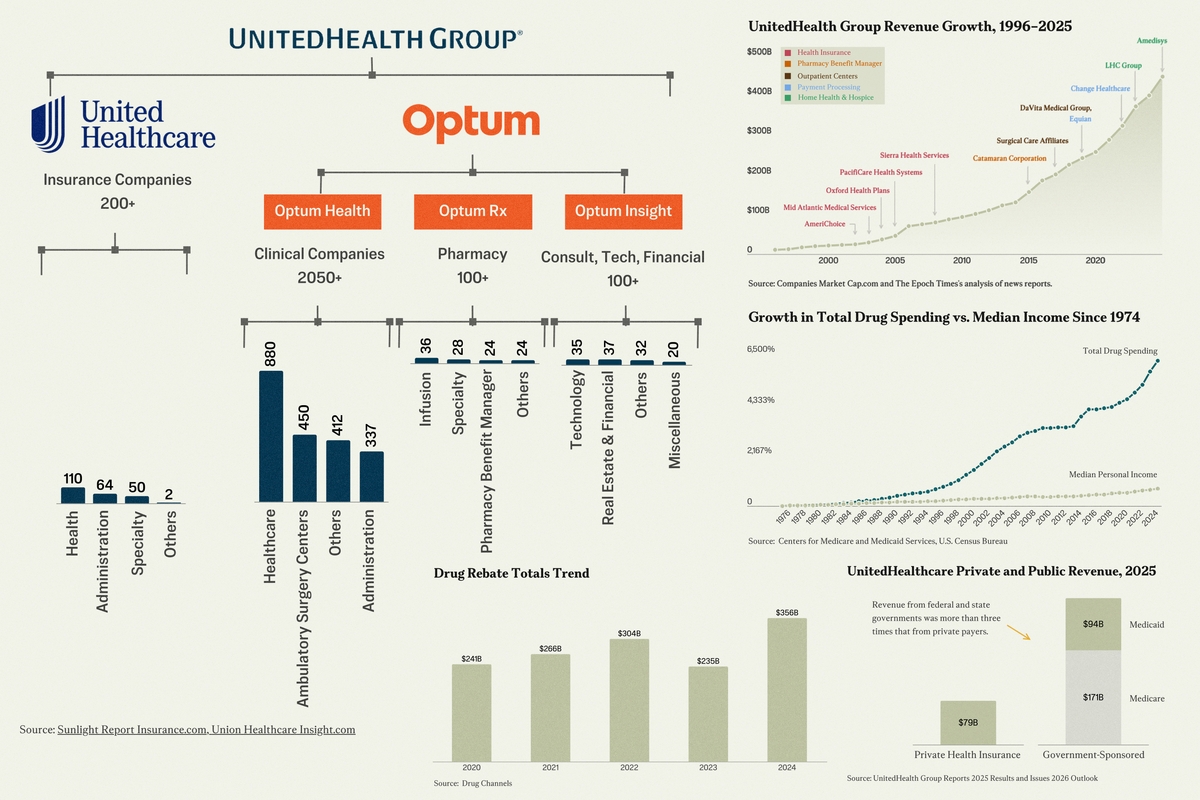

Established in the 1970s, UnitedHealth Group initially comprised a few health maintenance organizations, later expanding through acquiring insurance companies and medical service providers such as doctor’s offices and pharmacies.

In the early 2010s, Forbes ranked UnitedHealth Group as the 22nd largest company in the U.S.

However, a turning point came in 2015 when the company spent $13 billion to acquire the large drug benefit management company Catamaran. The drug benefit management company was a key independent player in the Medicare Part D market.

With the collapse of Catamaran, 80% of Medicare Part D patients were managed by three benefit management companies and their affiliated insurers.

The impact of this consolidation was immediate. Within a year, premiums for most customers saw an increase of up to 58%.

Research shows that even those who had previously used Catamaran’s services and continued with UnitedHealth Group post-consolidation did not see any cost savings.

“If you are the only game in town, you’re able to price things on your own, and there’s plenty of evidence out there that, in fact, it drives up costs,” said Elizabeth Mitchell, President and CEO of the Purchaser Business Group on Health based in Oakland, California, at a forum held by KFF in February.

According to company documents, UnitedHealth Group’s benefit management company, OptumRx, saw revenue growth of over 50% in the fourth quarter of 2015. Within just two years, UnitedHealth Group rose to rank sixth on Fortune’s list of the top 500 companies in America.

UnitedHealth Group has not responded to requests for comment.

During the years of continual price increases for brand-name drugs, there came a turning point.

From 2013 to 2021, brand-name drug prices under Medicare Part D increased by an average of 80%. As new drugs are typically expensive, the analysis considered only drugs sold throughout the entire period from 2013 to 2021.

This increase was nearly five times the rate of inflation and more than twice the growth in other drug expenditures.

During this time, spending on the insulin drug Humalog for Medicare increased by 86%, while spending on another insulin drug, Lantus, increased by 93%. The price of the blood thinner Eliquis rose by 123%.

The Federal Trade Commission in Washington, D.C., stated that this price surge was orchestrated.

The FTC accused UnitedHealth Group, CVS Health, and Cigna Group, along with their respective drug benefit management companies OptumRx, Caremark, and Express Scripts, of engaging in anticompetitive practices to inflate drug prices.

In 2024, the manufacturers spent a total of $356 billion in rebates and discounts.

In the 2024 fiscal year, following the second year of UnitedHealth Group, CVS and Cigna being subject to a $35 copayment for insulin in Medicare Part B and D, Humalog’s price dropped by 70%, while Novolog’s price dropped by 75%.

Taxpayers also bore a heavy burden. The majority of the income of the three major vertically integrated healthcare companies comes from government sources. So, any increase in drug prices impacts federal and state budgets.

From 2013 to 2023, Medicare Part D spending on brand-name drugs increased by over $100 billion.

Overall, by 2024, the U.S. healthcare spending on prescription drugs, including generic drugs, increased nearly 8% to reach $467 billion.

Taxpayers are the largest customers of UnitedHealth Group, accounting for about three-quarters of its revenue.

Vertical integration, according to the FTC, ultimately harms patients. This is because copayments are often calculated based on retail prices, so when prices rise, patients with high deductibles and copays end up paying more.

In some cases, patients may pay more for insulin than what their insurance company pays, as per a report by the Federal Trade Commission.

When dealing with vertically integrated companies, patients also see a reduction in their choices in the market. These companies often limit payments to medical institutions outside of their networks, guiding patients to use services from their affiliates.

While avocado sellers aim to increase customer loyalty by offering discounts, consumers dealing with vertically integrated companies can only utilize specific healthcare providers. People with employer-provided health insurance have their employers selecting the healthcare company, hospitals, doctors, mail-order pharmacies, and other service providers in the network.

According to a report from the House Committee on Oversight and Accountability, insurance companies might prevent patients from getting a 90-day supply of prescriptions from a competitor’s pharmacy or charge higher copays at non-affiliated pharmacies.

Research from the Washington State Pharmacy Association showed that using mail-order pharmacies in Washington state did not always reduce costs. The study found that in Washington, the cost of using a mail-order pharmacy was higher than that of a traditional pharmacy—even up to six times more for brand-name drugs.

The FTC stated that vertically integrated insurance companies sometimes pay higher drug prices to their affiliated mail-order pharmacies. Therefore, while patients may have lower copayments, the total cost borne by the premiums paid by the patients may actually be higher.

Proponents of vertical integration argue that this practice can reduce costs. The entire industry portrays itself as willing to take on pharmaceutical companies.

The Pharmaceutical Care Management Association based in Washington, D.C., claimed on its website that for every $1 spent on this service, there is a $10 reduction in costs.

“Integration should actually erode frictions, improve affordability, and streamline processes,” said Gail Boudreaux, CEO of Elevance Health based in Indiana, while addressing Congress on January 22.

However, Congressman Lloyd Smucker from Pennsylvania’s House Committee on Oversight and Accountability, shared on January 22 that, “if the market functioned properly, under consolidation in a highly concentrated market, premiums might decrease or at least see a slower growth rate.”

“But that is simply not the case.”

Caremark, Express Scripts, and OptumRx have agreed to settlements with the FTC in 2026, without admitting to any wrongdoing.

The preliminary settlement agreements announced by Caremark and Express Scripts reveal that they will agree to changes demanded by the FTC. These changes include basing deductibles and copayments on net prices rather than list prices for prescription drugs.

Meanwhile, in the decade post-acquisition of Catamaran, OptumRx’s revenue grew by 220%, adding approximately $10 billion annually.

UnitedHealth Group is now a holding company with around 2,700 subsidiaries, offering health insurance, drug benefit management, primary care, outpatient surgery, pharmaceutical sales, data analytics, real estate services, and managed healthcare services.

The annual revenue of the three major vertically integrated healthcare companies now exceeds $1 trillion.

These companies not only set prescription drug prices, claim rebates, and manage benefits but also, in many cases, prescribe medications and sell drugs to approximately 270 million Americans each year.