The Medicare Advantage plan in the United States, also known as Part C of Medicare, has been widely embraced by many beneficiaries as an alternative option to traditional Medicare. However, some experts have pointed out a hidden flaw within this plan that could potentially undermine the system.

People appreciate the Medicare Advantage plan because many of its offerings do not require additional payments beyond the standard Medicare Part B premium and provide benefits not included in traditional Medicare, while also lowering out-of-pocket costs. Currently, approximately 36 million Americans are enrolled in this plan.

However, there is a problem.

According to the Inspector General of the Department of Health and Human Services (HHS), a series of lawsuits filed by the Department of Justice (DOJ) have revealed an issue that has resulted in billions of dollars in losses for taxpayers.

In essence, to generate more revenue, insurance companies have been incentivized to enroll sicker patients into the Medicare Advantage plan. This has created a distorted incentive where the focus is on diagnosing illnesses rather than providing treatment.

By adding diagnoses in patients’ medical records that were never confirmed by a doctor, insurance companies can increase their revenue, even if the patients may have never received treatment for those conditions.

Four major insurance companies have reached settlements with the DOJ regarding this issue, while two cases are still pending.

This article delves into how the Medicare Advantage plan functions and why some experts believe this plan is vulnerable to manipulation.

Under the traditional Medicare system, patients see a doctor who then submits bills to Medicare for medical services provided. Medicare reimburses the doctor for these services in a fee-for-service model.

The Medicare Advantage plan operates differently.

In this plan, Medicare pays a set amount to insurance companies each month for each beneficiary’s healthcare costs, rather than paying for specific services rendered. This payment is based on a per-person model, similar to commercial health insurance.

When these individuals seek medical services, the insurance companies use the funds received from the government to cover these costs.

This model closely mirrors how commercial health insurance operates, where policyholders pay premiums, and the insurance company covers medical expenses beyond deductibles and copays by charging a set fee to assume part of the risk.

However, a key distinction between Medicare Advantage and commercial health insurance is how risk adjustment is handled within the plan.

Risk under Medicare Advantage can be adjusted throughout the year based on changes in beneficiaries’ health. For instance, if a 65-year-old in average health living in the Midwest would have Medicare pay the insurance company $1,000 per month, that payment could increase by $200 per month if they are diagnosed with diabetes in April.

This adjustment is known as risk adjustment.

If a beneficiary is diagnosed with a new illness during the year, the insurance company can receive additional payments based on that diagnosis.

At this point, Medicare Advantage differs significantly from traditional Medicare and commercial health insurance.

Typically, individual and small group insurance rates are primarily based on a few factors like the insured’s location and age, while rates for large group insurance consider the experience of the entire group insured.

However, insurance companies cannot raise premiums mid-year due to one insured individual becoming ill. By federal law, they are not allowed to change premiums solely based on one person’s diagnosis.

Some experts argue that it is this loophole that makes the Medicare Advantage plan susceptible to abuse.

According to the DOJ, at some point, insurance companies began manipulating patient data by adding diagnoses – often conditions that were never diagnosed by a doctor – artificially increasing patients’ risk scores.

Therefore, insurance companies could receive more money regardless of whether the beneficiary had received treatment for the condition, or even if they were aware of having that illness themselves.

If it turned out that these beneficiaries’ conditions were indeed more severe than they or their doctors had realized, this would indeed pose additional risks for the insurance companies.

However, even if it was later discovered that these added diagnoses were inaccurate, some insurance companies had never removed them from the patients’ records or refunded the overpayments made for providing medical services.

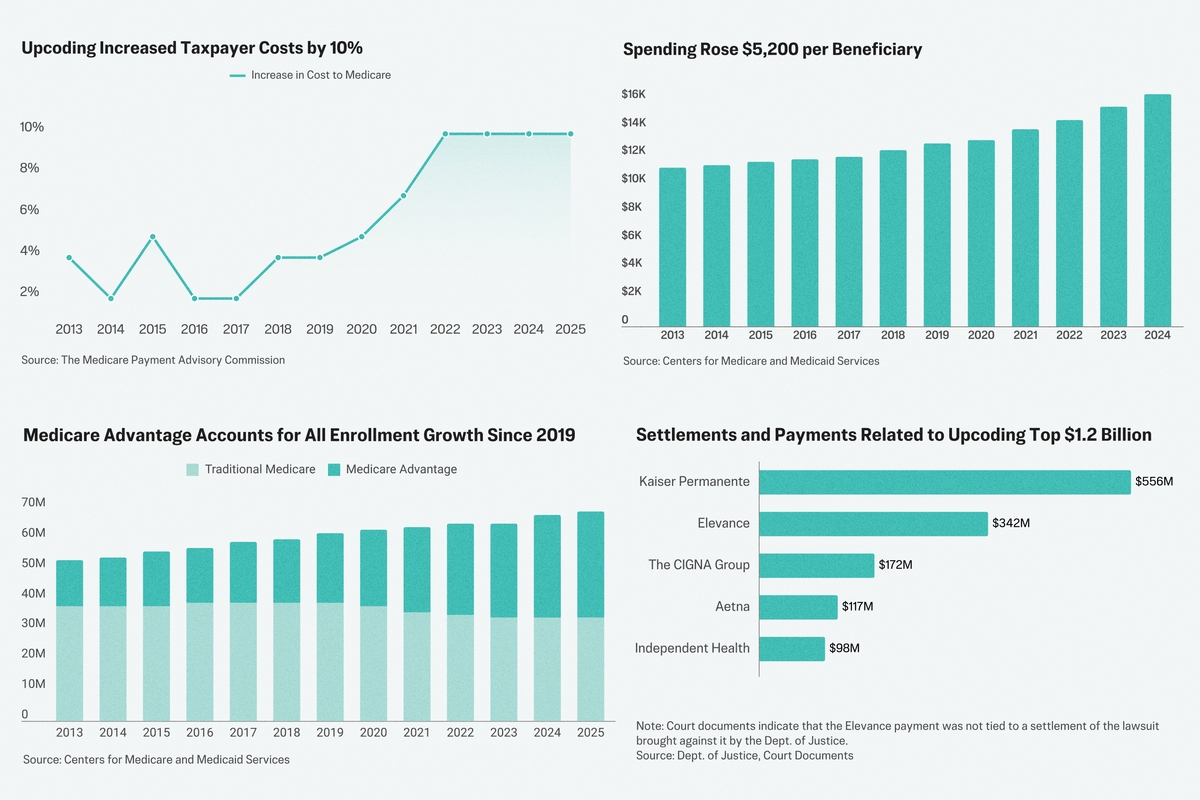

According to the Office of Inspector General, diagnoses determined through data – those appearing only in the company’s risk assessment and not in patients’ medical records – cost taxpayers $7.5 billion annually. Certain chronic illnesses like diabetes and congestive heart failure increase payment costs after risk adjustment.

An audit of 97 insurance beneficiaries classified as high risk for strokes found that all submitted diagnosis codes lacked supporting evidence in doctors’ records. A report from the Inspector General’s Office in May indicated that this led to taxpayers losing approximately $462 million in overpaid insurance funds.

Ultimately, whistleblowers within six insurance companies discovered this practice and initiated lawsuits against them, which the DOJ subsequently joined. The lawsuits allege that major insurance companies like UnitedHealth Group, Cigna, Independent Health, Elevance (formerly Anthem), Aetna, and Kaiser Permanente engaged in upcoding practices.

The first lawsuit initiated by a whistleblower began in 2011. While four cases have been resolved, two are still pending, including the initial lawsuit against UnitedHealth Group.

Some cases of insurance companies accused of upcoding diagnoses include:

– Kaiser Permanente, a large healthcare company, allegedly instructed doctors to add additional diagnostic results to patients’ medical records.

– CVS Health’s insurance company, Aetna, reportedly paid coding specialists to review patients’ medical histories to identify potential diagnoses that could support additional codes submitted to Medicare and Medicaid.

– Aetna was found to have diagnoses lacking data support but did not remove them as required by regulations or return funds to Medicare.

– Allegations of up to six years of improper diagnoses were made against UnitedHealth Group, leading to billions in increased payments and failure to refund at least $1 billion in improper payments.

Despite these issues, some industry analysts view risk adjustment as a beneficial mechanism overall.

Supporters argue that risk assessments by insurance companies can provide early warnings for chronic diseases and prevent conditions from worsening.

The CMS notes, “Risk adjustment ensures accurate payments to insurance companies based on the health status of the beneficiaries, thereby strengthening [Medicare Advantage].”

However, some believe it is a way for large, data-savvy corporations to increase profits at the expense of taxpayers.

Senator Charles Grassley, a Republican from Iowa, expressed concerns about potential abuses within the system, emphasizing the need for an accurate and fair risk adjustment process for taxpayers and patients to benefit from Medicare Advantage.

UnitedHealth Group stated in a 2025 release, “We are firmly committed to the integrity of our Medicare Advantage business and the positive impact it has on millions of older Americans nationwide.”

Some experts argue that the real issue lies in serious flaws within the Medicare Advantage plan itself.

The Bipartisan Policy Center in Washington, D.C., mentioned that it continues to provide economic incentives for medical service providers participating in the plan to document all possible diagnoses for their beneficiaries.

The Alliance of Community Health Plans in Washington, D.C., CEO Ceci Connolly, stated in 2025, “The concept of risk adjustment was good initially, but it has spiraled out of control and been widely abused. This is a system failure.”

As of March of this year, 36 million people are enrolled in Medicare Advantage, with an annual payment exceeding $500 billion when calculated around $14,000 per capita.

The Commonwealth Fund in New York indicated that federal officials are considering reforms to curb exaggerated risk assessment results. These reforms include extending the timeframe for risk assessment from one year to two years and inferring diagnoses based on actual service claims provided.

In January of this year, Kaiser Permanente reached a settlement with the U.S. Department of Justice, agreeing to pay a $556 million fine without admitting wrongdoing.

Kaiser Permanente issued a statement emphasizing that the dispute revolved around the interpretation of federal risk adjustment requirements.

In March, Aetna reached a settlement with the government and stated that they do not agree with the DOJ’s industry-wide charges, with the settlement not indicating acknowledgment of liability. Aetna agreed to pay $117 million to the government.

Cigna Group and Independent Health settled similar lawsuits in 2023 and 2024, respectively. Both companies agreed to pay $172 million and $98 million to resolve the allegations of upcoding diagnoses.

The companies did not admit to any wrongdoing and signed five-year agreements with the government to implement accountability and auditing measures.

The lawsuit against Elevance is still ongoing, with allegations that the insurance company illegally obtained and retained millions of dollars under the risk adjustment payment system.

UnitedHealth Group also faces similar claims, with allegations of increasing risk-based payments by approximately $3 billion over six years and failing to refund at least $1 billion in improper payments.

In March 2025, a specially appointed magistrate recommended a summary judgment favoring UnitedHealth Group, stating that the government failed to prove its allegations.

The case is currently in the ongoing litigation process.