Xinjiang Daquan New Energy Co., Ltd. (Daquan Energy) has suffered losses totaling more than 3 billion RMB in 2024 and the first quarter of this year, causing the chairman and his son’s net worth to shrink to 10 billion RMB. The main reason for the losses is that the selling price of the company’s products, polycrystalline silicon, has dropped by over 70%.

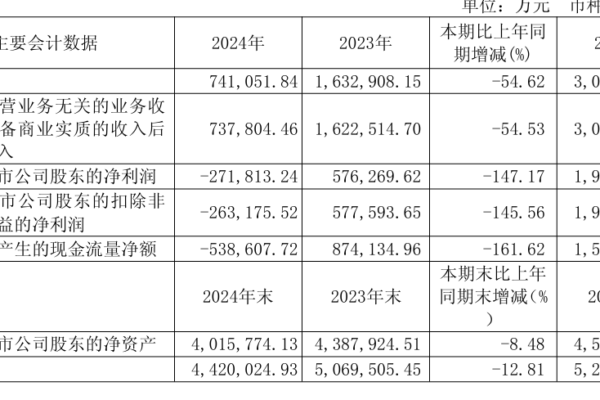

The annual reports for 2024 and the first quarter of this year released recently show that Daquan Energy incurred losses of 2.7 billion RMB and 560 million RMB respectively.

According to the Hurun Global Rich List 2025, the actual controllers of the company, father Xu Guangfu and son Xu Xiang, have seen their wealth shrink to 10 billion RMB.

A report by “21st Century Business Review” on May 31st pointed out that the plummeting price of polycrystalline silicon has led to the distress of Daquan Energy.

From 2022 to 2023, the selling price of polycrystalline silicon dropped from 266 RMB/kg to 81 RMB/kg. By the end of March 2025, the selling price of Daquan Energy’s polycrystalline silicon fell below 32 RMB/kg, below the cash cost line of 36.8 RMB/kg, resulting in a loss of 4.8 RMB/kg.

The price collapse caused a 70% year-on-year decline in income for the Xu family from January to March.

In response to the price drop, Daquan Energy has started to control production capacity and stated: “The company plans to maintain a relatively low capacity utilization rate in 2025 until the industry reaches a turning point.”

However, facing industry-wide overcapacity, the short-term situation for the industry is unlikely to improve. Lv Jinbiao, an expert from the Silicon Industry Branch of the China Nonferrous Metals Industry Association, stated: “It is projected that global polysilicon capacity will reach 3.5 million tons in 2025, while demand is around 1.77 million tons.”

By the end of 2024, Daquan Energy’s polycrystalline silicon production capacity reached as high as 305,000 tons, approximately double that of two years ago. In the first quarter of this year, the company’s polycrystalline silicon production was only 25,000 tons.

In its annual report, Daquan Energy stated, “If production capacity continues to increase or downstream companies adjust procurement strategies, there is a risk of continued decline in polycrystalline silicon prices.”

During the performance meeting on May 29, the management of Daquan Energy once again stated that the supply and demand situation for silicon material has not significantly improved, and in the short term, there is limited upward momentum for silicon material prices.

Since the beginning of 2022, Daquan Energy’s stock price has plummeted from 56 RMB/share to below 20 RMB/share, evaporating nearly 78 billion RMB in market value.

As of 15:30 Beijing time on May 30, Daquan Energy’s stock price was reported at 19.25 RMB/share, a decrease of 0.62%, with a total market value of 41.295 billion RMB.

Xinjiang Daquan New Energy Co., Ltd. was founded in February 2011, primarily engaged in the research and development, production, and sales of high-purity polycrystalline silicon material. The company was listed on the Shanghai Stock Exchange’s Sci-Tech Innovation Board on July 22, 2021.

Public data shows that polycrystalline silicon is the main raw material for manufacturing photovoltaic cells, with almost no mature alternative.