In the first half of 2025, JA Solar Technology Co., Ltd. (JA Solar), a company from mainland China, reported a net loss of 2.909 billion yuan (RMB), compared to a profit of 1.2 billion yuan in the same period last year, marking a significant shift from profit to loss. Data indicates that the entire solar industry in China is facing serious overcapacity issues, with companies struggling to navigate through challenging times.

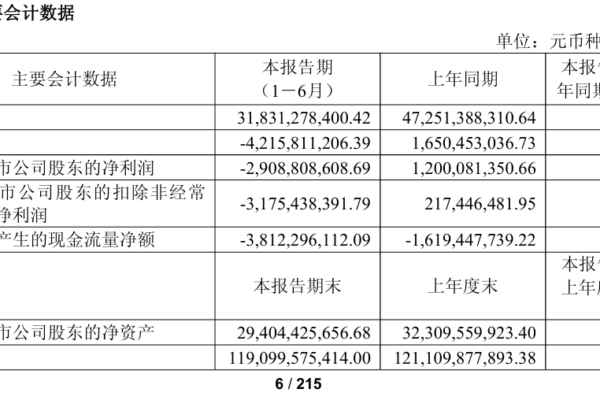

On August 28th, JA Solar released its “2025 Semi-Annual Report,” revealing that the company achieved a revenue of 31.831 billion yuan, a decrease of 32.63% compared to the previous year. The net profit attributable to shareholders was -2.909 billion yuan, a decrease of 342.38% year-on-year, with profits turning into losses. The non-GAAP net profit (net profit excluding non-recurring gains and losses) was -3.175 billion yuan, a decrease of 1560.33%.

Regarding the first-half loss, JA Solar attributed it to intensified competition in the solar market, leading to continuous decline in solar product prices and a subsequent drop in the company’s main business revenue.

The report also indicated that the company generated a net cash flow from operating activities of -3.812 billion yuan in the first half of the year, mainly due to a decrease in sales receipts during the reporting period. Additionally, research and development expenses decreased by 56.95% compared to the same period last year. The total assets amounted to 119.1 billion yuan, a 1.66% decrease from the previous year-end, while the net assets attributable to the company’s shareholders stood at 29.404 billion yuan, an 8.99% decrease from the previous year-end. The asset-liability ratio was 74.07%, a 2.08 percentage point increase from the previous year-end, exceeding the industry average.

According to public data, JA Solar Technology Co., Ltd. is a photovoltaic enterprise involved in the research, processing, manufacturing, installation, and sales of monocrystalline silicon rods, monocrystalline silicon wafers, polycrystalline ingots, polycrystalline silicon wafers, high-efficiency solar cells, modules and photovoltaic application systems, as well as the production and sales of solar raw materials and related supporting products.

Radar Finance, a subsidiary of Beijing Xuelang Technology Co., revealed on August 30th that many companies in the solar industry have been facing difficult times in recent years. According to data from the China Photovoltaic Industry Association, in the first quarter of 2025, the overall net losses of 31 A-share listed companies in the photovoltaic main industry chain reached a staggering 12.58 billion yuan, a 274.3% year-on-year increase in loss levels.

In the first half of this year, leading photovoltaic giants such as Longi Green Energy, GCL System Integration, JA Solar Technology, and Tongwei Co., Ltd. also suffered significant performance setbacks. The net profits attributable to shareholders of these companies were -2.569 billion yuan, -2.918 billion yuan, -2.58 billion yuan, and -4.955 billion yuan, respectively.

Starting from 2024, prices in various segments of the photovoltaic industry chain began to enter a downward trend, which continued unabated in the first half of this year. In a bid to grab market share, many companies adopted price reduction strategies, intensifying industry competition.

Moreover, there is severe overcapacity in the solar industry. According to data released by the industry authority InfoLink Consulting, as of the end of 2024, Chinese manufacturers’ capacities for silicon materials, silicon wafers, cells, and modules all exceeded 1,100GW (1 gigawatt = 1,000 megawatts), while optimistic demand projections for 2025 globally and in China were only 600GW and 250GW, respectively.

During a seminar on the review of the development of the solar industry in the first half of 2025 and the outlook for the second half, Wang Bohua, Honorary Chairman of the China Photovoltaic Industry Association, admitted that the first half presented significant challenges for the Chinese photovoltaic industry.

Wang Bohua stated that in the first half of this year, the production growth of cells and modules had dropped to below 15%, with polycrystalline silicon and silicon wafers even experiencing negative growth. The price decline was even more pronounced, with the prices of mainstream models in three segments reduced by over 80% compared to the highest prices since 2020.

Radar Finance indicated that since 2024, over 40 photovoltaic companies have announced delisting, bankruptcy, or undergone mergers and acquisitions, as per incomplete statistics.