In recent times, Chinese listed photovoltaic (solar energy) companies have successively released their 2024 annual reports, which reveal that in the past year, these companies have faced severe challenges, marking the worst performance in their history.

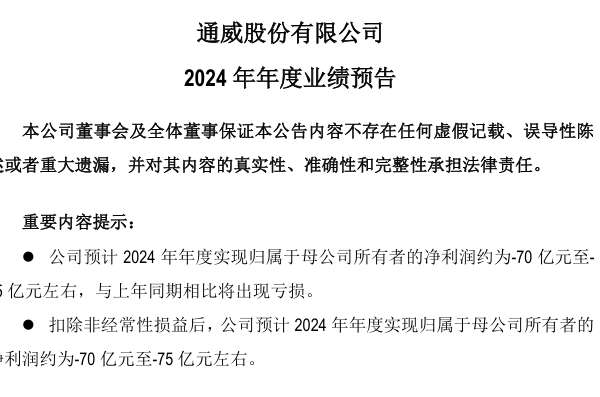

On the evening of January 17th, leading integrated PV company Tongwei Group announced in its “Tongwei Group Co., Ltd. 2024 Annual Performance Forecast” that it is expected to incur a net loss attributable to the parent company of approximately 7 to 7.5 billion yuan in 2024, compared to a profit in the same period last year.

This will be the first annual loss for Tongwei Group since 2000. Chairman of Tongwei Group, Liu Hanyuan, had previously expressed that if the full-year performance remains in the red, it will be the first annual loss for Tongwei in the A-share market in 23 years of its listing and the first loss in its 42-year history.

Explaining the reasons for the losses, Tongwei Group stated that in 2024, market prices in various segments of the PV industry chain saw significant declines, even falling below the industry’s cash cost for some periods, coupled with the impact of approximately 1 billion yuan from long-term asset impairment and write-offs throughout the year, resulting in a full-year loss.

According to The Paper, the PV industry in China experienced unprecedented turbulence in 2024, surpassing industry expectations. With the release of 2024 performance forecasts, several PV companies have delivered their worst annual reports in history.

On January 16th, another leading integrated PV company, Longi Green Energy, announced that it expects to incur a net loss attributable to shareholders of the listed company between 8.2 and 8.8 billion yuan in 2024.

In 2023, the company achieved a net profit attributable to its parent company of 10.751 billion yuan. Historical data shows that a net loss exceeding 8 billion yuan is the second annual loss for Longi Green Energy since 2007 and its largest annual loss in history.

Moreover, known as the “top PV stock” on A-share market, JA Solar’s announcement on January 14th estimated a net loss of 1.9 to 2.3 billion yuan in 2024, switching from profits to losses compared to the same period last year, and is expected to mark the highest annual loss in the company’s history.

Another PV company, Chint Solar, expects a net profit of 280 million to 340 million yuan for the previous year, a year-on-year decrease of 93.25% to 94.44%; excluding non-recurring profits of 231 million to 291 million yuan, a year-on-year decrease of 94.21% to 95.40%.

Regarding the reasons for last year’s losses, Chint Solar explained that the drastic fluctuations in the PV industry market were influenced by excess production capacity and inventory clearance activities, coupled with a significant decrease in demand for PV quartz materials, resulting in a substantial decline in the company’s operational performance.

Apart from PV companies, upstream enterprises also experienced losses.

An announcement by Daqo Energy on January 17th showed that it is expected to incur a net loss attributable to the company’s owner of 2.6 to 3.1 billion yuan in 2024, compared to the same period last year.

Daqo Energy attributes the losses to the significant supply-demand imbalance in the polysilicon market in 2024, leading to an ongoing decline in product prices below industry cash costs, causing a substantial drop in overall industry gross and profit margins. Additionally, the company made provisions for inventory write-downs and conducted impairment tests on non-current assets, resulting in a significant impact on its performance for the reporting period.

Established in February 2011, Daqo Energy’s net loss in 2024 is its worst performance in over a decade.

On January 17th, PV equipment manufacturer, “Silicon Slice Newcomer,” Hon-Link New Energy, announced an expected net profit attributable to the parent company’s owner of -2.5 to -2.7 billion yuan for 2024. In 2023, the company’s net profit was approximately 741 million yuan. This marks the first annual net profit loss for Hon-Link New Energy since 2009.

Hon-Link New Energy attributed its performance to fierce market competition within the PV industry, influenced by factors such as oversupply in the industry, intensified competition, and continuous downslide in product prices along the PV industry chain, leading to declining sales revenue and reduced profitability.

Similarly, PV material manufacturer Sunport Technologies fell into losses. Sunport Technologies, the leading PV backboard company, issued a performance forecast on January 16th, predicting a net profit attributable to the parent company’s owner of -250 to -200 million yuan in 2024. In 2023, its net profit was around 104 million yuan.

Sunport Technologies mentioned that performance losses were mainly due to the impact on PV material business. During the reporting period, changes in supply-demand relationships in the PV industry, the transmission of price pressures along the industrial chain, and intensified market competition led to decreased demand and unit prices for PV backboards, stabilizing sales volume for PV films but with declining product prices, resulting in a year-on-year decrease in operating income and profit levels.

Chairman of the China Photovoltaic Industry Association, Wang Bohua, stated at an industry forum in early December last year: “The losses caused by this industry turbulence far surpass the three previous industry turbulences (the 2008 financial crisis, the ‘double reverse’ in 2012, and the industry policy adjustments in 2018).” From January to October last year, as the manufacturing, application, and export volumes of the PV industry expanded, prices, manufacturing output values, and export figures of the industry chain significantly decreased. Prices in all segments dropped by 60% to 80% compared to the peak in 2023, with the PV manufacturing output value declining by over 44.7% in the first three quarters, exceeding 570 billion yuan; losses for PV enterprises continued to widen, with 39 out of 121 listed PV companies recording net profit losses, and leading companies facing more severe losses.

Additionally reported on Caixin Net on January 18th, among the top companies in the PV industry with severe losses, a total of 15 top chain companies experienced losses, with a generally over 100% year-on-year decline in net profits.

Regarding exports, the PV industry saw an increase in volume while revenue decreased. According to the China Customs Administration’s December statistical monthly report updated on January 18th, China exported 820 million solar cells in December, an 82.8% increase year-on-year, but export revenue decreased by 16% to $1.958 billion; with total annual solar cell exports of 7.79 billion in 2024, a 38.2% increase year-on-year, amounting to $30.598 billion, a 30% decrease compared to the previous year.

Chinese financial expert Xu Zhen told The Epoch Times that the issue of intensified competition within PV companies is mainly determined by the nature of the PV industry itself. China’s massive production capacity saturates the European and American markets after a while. When PV companies face severe overcapacity, they will encounter fierce competition and internal convergence.

Xu Zhen believes that due to China’s rich coal resources in Xinjiang, the low cost of electricity generation, and most polysilicon production taking place in the Xinjiang region, if the United States bans the import of Xinjiang cotton and PV products to sanction the Chinese Communist Party’s human rights abuses, the European Union is likely to follow suit, which will lead to a wave of closures in the mainland PV industry shortly.