In order to stimulate the sluggish real estate market, several cities in China have recently introduced “zero down payment” policies for buying houses, prompting caution among potential buyers.

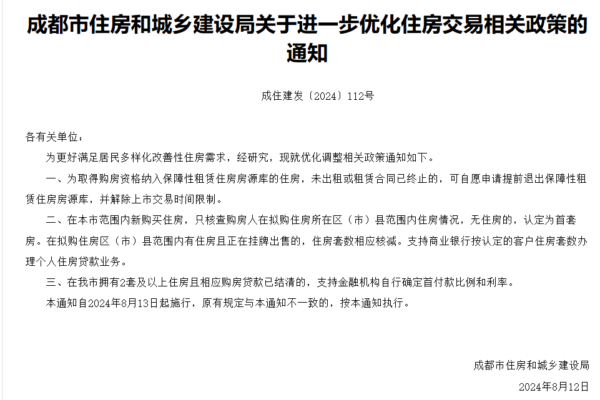

The Housing and Urban-Rural Development Bureau of Chengdu, China, issued a notice on August 12 titled “Notice of Further Optimizing Housing Transaction Policies in Chengdu”. The notice indicates that “For those who own two or more properties in our city and have already repaid the corresponding mortgage loans, financial institutions are allowed to determine the down payment ratio and interest rates themselves.”

In simple terms, this means that financial institutions in Chengdu can decide the down payment ratio for purchasing a house, including the possibility of zero down payment.

This practice of zero down payment for purchasing homes is not limited to Chengdu; it is also observed in cities like Shenzhen, Guangzhou, Hangzhou, and Changsha.

In China, during periods when the real estate market is in a downturn, zero down payment schemes tend to emerge discreetly. Despite being against regulations, there is demand from buyers, developers need to sell properties, and banks aim to make profits. Therefore, developers utilize zero down payment schemes as a strategy to attract more buyers.

However, Jiang Hao, a financial expert in Mainland China, cautioned potential buyers considering zero down payment schemes to be vigilant.

Jiang Hao explained that there are currently three main ways to carry out zero down payment purchases.

The first method involves inflating the property valuation in order to obtain a higher loan amount, resulting in increased monthly repayments.

The second method entails finding a third party to fund the down payment temporarily, with the buyer eventually repaying this amount through various loan channels.

Jiang Hao pointed out that both of these methods are considered rule-breaking practices. However, during the real estate market slump, many regions and banks tend to turn a blind eye to such practices due to the existing demand.

While these operations benefit developers and banks financially, they also increase the repayment burden on buyers. Jiang Hao advised potential buyers to refrain from zero down payment schemes, especially if they are financially constrained.

Furthermore, buyers are urged to consider local policies supporting zero down payment purchases. Undertaking such schemes in areas where it is not officially supported can pose risks such as investigations or requirements to repay portions of the loan prematurely.

Many netizens have also expressed concerns about zero down payment purchases being a potential trap, where both the down payment and monthly installments could result in financial losses.

A user on Tencent’s platform commented that the absence of a down payment reflects poor economic conditions, emphasizing the importance of maintaining a safety buffer in repayments.

Another netizen emphasized the strategic advantage of sellers over buyers in such scenarios, with a continuous stream of new tactics being employed by them.