On August 12, the city of Chengdu announced a new policy for the qualification of the first-home buyers, which has received comments from industry insiders suggesting that it is “almost equivalent to ‘no house, no loan'”.

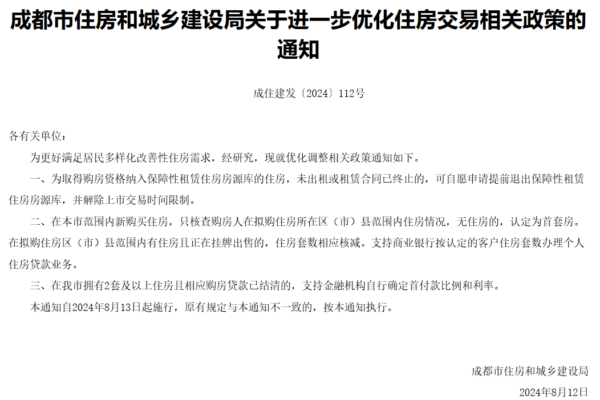

The Chengdu Housing and Urban-Rural Development Bureau issued a notice titled “Notice on Further Optimizing Policies Related to Housing Transactions” on its official website on August 12. According to the notice, for newly purchased houses within the Chengdu area, only the housing situation within the district where the house is located will be examined to determine if it is the first-home purchase. If no housing is owned within the district where the house is to be purchased, it will be recognized as the first-home purchase. If there are owned houses within the district where the house is to be purchased and they are listed for sale, the number of housing units will be deducted accordingly. Commercial banks are allowed to process personal housing loans based on the recognized number of housing units of the customers.

Furthermore, for individuals in Chengdu who own two or more housing units and have paid off the corresponding housing loans, financial institutions are allowed to determine the down payment ratio and interest rates independently.

This notification will come into effect from August 13, 2024.

In response to this, Caixin explained that the so-called first-home qualification mainly affects the loan-to-value ratio and interest rates for home buyers, involving the terms “recognize the house” and “recognize the loan”. Typically, “recognizing the house” refers to commercial banks considering the number of housing units owned by the buyer in the local area when determining the loan-to-value ratio. The loan-to-value ratio for the first-home purchase is higher while it is lower for the second home, resulting in increased down payment costs. “Recognizing the loan” refers to banks determining the loan-to-value ratio based on whether the buyer has a housing loan record nationwide. Currently, in China, various cities generally implement the policy of “recognize the house but not the loan”, meaning that as long as the buyer does not own any property locally, they can be recognized as buying the first home and can purchase at a lower down payment ratio.

Regarding Chengdu’s relaxation of real estate policies, a Chengdu intermediary told Caixin that it is “almost equivalent to ‘no house, no loan'”, and as long as the owned house is listed, they can apply for a loan according to the standards of the first-home purchase, even if “multiple houses under the individual’s name without a mortgage can be recognized as the first home”.

As we enter 2024, the Chinese real estate market remains sluggish, with a continuous decline in the national volume of new home transactions and a general decline in the volume of second-hand home transactions outside of certain popular cities. According to data from Zhongzhi Research Institute, a market research organization, from January to July, the number of new home transactions in key monitored cities all declined year-on-year, with only Shenzhen, Hangzhou, Qingdao, and Shanghai showing an increase in the number of second-hand home transactions, while other cities experienced a decrease. Specifically, the number of new and second-hand home transactions in Chengdu from January to July declined by 39% and 9% respectively.